Top Five Spenders

The top five government spenders on emergency arts funding packages (out of the 54 countries I have found info for) are:

Austria (EUR 2 billion for arts and culture) (c. 8.9 million population; EUR 225 per capita)

Poland (EUR 900 million for arts and culture) (c.38 million population; EUR 24 per capita)

Japan (EUR 882.2 million, mostly for global demand creation and promotion of content) (c. 126.5 million population, EUR 7 per capita)

Netherlands (EUR 300 million for arts and culture) (c. 17.3 million population, EUR 17 per capita)

USA (EUR 282.9 million for arts and culture) (c. 328.2 million, EUR 0.86 per capita)

NOTES: This is for emergency funding - I am waiting for more countries to make announcements before I do a comparison. Germany is probably the top of this list, but they have included arts in an overall EUR 50 billion package for small businesses so I can't tell how much is going to the arts yet. Canada may also make it into the top five, but it is not clear how much of their EUR 328 million fund for culture, heritage and sport is going to arts/culture. If we include recovery spending, New Zealand is in the top five for funding calculated per capita.

MY ANALYSIS

Five types of good practice

I wrote an article analysing the international government responses to the impact of COVID-19 on the arts and cultural sector. In the article, I identified the following aspects of ‘good practice’ in governmental support for the arts and cultural industries:

Money (preferably lots, and with the possibility of more), targeted at the arts and creative industries across the supply and demand value chain (educators, independents, institutions, meditators, critics, curators, distributors, presenters…)

Support for the self-employed and freelancers.

Direct support without paperwork.

Digital and other programs which work with the current environment.

Support the public to access the arts and culture during lockdown.

What governments are doing (in brief)

First wave of economic stimulus (c. March): a lot of the government measures in the first wave of economic measures targeted small to medium businesses, including rent and tax relief, cash grants and low-cost loans

Second wave of economic stimulus (c. April): Governments then tended to offer support for the unemployed, including helping businesses to keep people employed at lower rates of pay. Many countries specifically extended social insurance schemes to artists and freelancers, recognising they often fall through the cracks of general economic measures.

Third wave of economic stimulus (c. April-May): Many governments also provided extra subsidies directly to arts and cultural organisations to prevent them from closing. Some governments also re-directed funding to provide individual artists with additional grant opportunities.

Access to culture during lockdown (c.March-ongoing): digital programs are popping up across a number of jurisdictions to support artists to create digital content. Countries like Egypt, Indonesia, Poland and Chile are also setting up digital aggregators of arts content so the public can still access cultural content during lockdown.

Shift to recovery (May-ongoing): Governments are also beginning to develop recovery packages and responses. This includes New Zealand’s NZ $175 million over three years to re-start the arts sector, and Germany’s EUR 1 billion (yes, billion) in ‘Neu Start’ for culture.

Reasons to support the creative industries

It’s worth remembering that the global creative industries contribute $2.25 trillion USD to the world economy annually - approx. 3% of world GDP - and 29.5 million jobs around the world.

The next wave of support will be vital for the arts and cultural sectors, given that in Australia, for example:

76% of artists are freelancers

Four in five artists take on non-arts related work to make ends meet

60% of creative industry businesses have no employees, whilst 39% have fewer than 20 employees

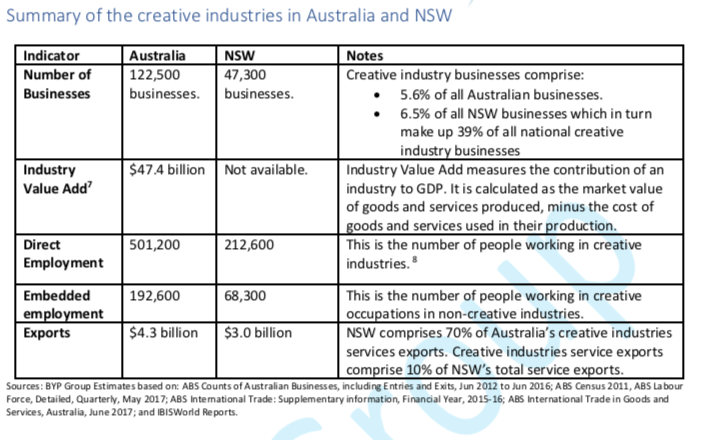

In Australia, creative industries comprise 6% of all businesses and employment, contribute $47.4 billion to national GDP, employ more than half a million people and generate $3.2 billion in export revenue.

Creative industries employment is growing faster than employment in the rest of the economy

Sources - BYP Group report on NSW creative industries; Throsby report on artists, reports from QUT, Creative Industries Innovation Centre and EY.

There is also the critical issue of mental health and wellbeing. Artists work in precarious environments with multiple stressors. By dint of being creative types, we so often take the world’s malaises and internalise them. Remember:

RUOK?

Call someone every day even if you don’t feel like it. Touch base.

Things always look better after a nap or a walk. Preferably both.

There are free government-supported mental health counselling. Even if you are physically alone, you are not alone in how you feel. We will make it together. Take care, keep going.

GOVERNMENT RESPONSES FOR THE ARTS AND CREATIVE INDUSTRIES

Argentina

Recovery Approaches

We are not aware of any announcements as at 11 June 2020.

Digital Actions

In April 2020, the Ministry of Culture Argentina announced ARS $7.2 million for hiring nearly 500 artists to develop content for ‘Culture at Home’ through the digital platform Formar Cultura, which is a virtual community of practice.

Emergency Support

In April 2020, the Ministry of Culture Argentina has announced:

The Culture Points Program will have its budget increased from 17 to 50 million pesos

30 million pesos in emergency funds for cultural centres

The National Commission of Public Libraries will increase investment in the book program for the purchase of books. The funds earmarked for the Book Fair will be redirected to this.

The National Theatre Institute will allocate 96 million pesos for studios, plays and festivals

The National Arts Fund will boost the payment of scholarships, competitions, subsidies and loans with 22 million pesos, and launch a new call with funding of 75 million pesos

The National Institute of Music is extending the deadline for financial acquittals

The Infanto Juveniles Orchestras program will have 9.2 million pesos for new instruments

7.2 million pesos for hiring nearly 500 artists to develop content for ‘Culture at Home’ through the digital platform Formar Cultura, which is a virtual community of practice

Visit the website for more info.

Australia

Recovery Approaches

25 June, The Australian Prime Minister announced a $250 million support package for Australia’s art and cultural sectors. The new grants and loan programs will be rolled out over the next 12 months and includes:

Seed Investment to Reactivate Productions and Tours – $75 million in competitive grant funding in 2020- to help production and event businesses to put on new festivals, concerts, tours and events as social distancing restrictions ease, including innovative operating and digital delivery models. Grants will be available, from $75,000 through to $2 million.

Show Starter Loans – $90 million in concessional loans to fund new productions and events that stimulate job creation and economic activity.

Kick-starting Local Screen Production – $50 million for a Temporary Interruption Fund, to be administered by Screen Australia, that will support local film and television producers to secure finance and start filming again.

Supporting Sustainability of Sector-Significant Organisations – $35 million to provide direct financial assistance to support significant Commonwealth-funded arts and culture organisations facing threats to their viability due to COVID-19, which may include organisations in fields including theatre, dance, circus, music and other fields. The Government will partner with the Australia Council to deliver this funding.

Creative Economy Taskforce – establishment of a ministerial taskforce to partner with the Government and the Australia Council to implement the JobMaker plan for the creative economy

For further details and to read the media release click here

Digital Actions

On 24 April, the Australian Broadcasting Corporation (ABC) announced a AUD $5 million “Fresh Start Fund” for development, and includes an Arts Digital Fund with a focus on documentary storytelling, and an Australian Music fund.

Emergency Support

In Australia, the Federal government has announced a $168 billion stimulus package. Here’s what is relevant to the arts and creative industries:

Businesses and NFPs with turnover under $50 million and that employ people can access $20,000-$100,000 to keep operating and keep staff. There is also support available to retain apprentices and trainees.

The Government is allowing businesses and not-for-profits impacted by the Coronavirus to access a subsidy to continue paying their employees. The JobKeeper payment allows affected employers to claim $1,500 a fortnight per eligible employee for a maximum period of six months. Creative and cultural businesses are eligible.

Government is increasing the threshold at which creditors can demand payment and offering temporary relief for directors from personal liability for trading while insolvent.

$1 billion to support regions, communities and industries severely affected by COVID-19, ‘including those heavily reliant on industries such as tourism, agriculture and education.’

From April 27 2020, sole traders, self-employed, contract and casual workers who meet the income tests as a result of the economic downturn due to COVID-19 can access Jobseeker Payment and Youth Allowance Jobseeker. This could also include a person required to care for someone affected by COVID-19. People on these payments will also receive an extra $550 per fortnight COVID-19 supplement, and two x one-off payments of $750. Asset testing for these payments and the Parenting Payment will be waived for the period of the COVID-19 supplement. The Liquid Asset test Waiting Period will also be waived for recipients eligible for the COVID-19 supplement.

Sole traders accessing Jobseeker Payment will automatically meet the usual requirements of the Payment by continuing to develop their business.

Individuals can also access up to $10,000 of their superannuation in 2019-20 and a further $10,000 in 2020-21.

Increased instant asset write-off - individual assets threshold raised from $30,000 to $150,000.

Accelerated depreciation deductions for businesses with a turnover of less than $500 million can deduct 50% of the cost off an eligible asset on installation.

On 9 April the government also announced AUD $27 million for First Nations arts, regional arts and the music charity Support Art:

$10 million to Support Act

$10 million through the Regional Arts Australia’s Regional Arts Fund

$7 million through the Indigenous Visual Arts Industry Support Program

The government has also brought forward AUD $5 million from its Regional and Small Publishers Innovation Fund to support public interest journalism during COVID-19. More organisations are eligible to apply and there is a greater emphasis on sustainability.

The Australia Council for the Arts has announced:

A “Resilience Fund" which is a repurposing all uncommitted funds from 2019-20 to immediately respond to the crisis, redirecting $5 million AUD to new programs designed to provide immediate relief for artists and organisations. The Fund has three streams:

Survive - small grants or individuals, groups and organisations to offset or recoup financial losses due to cancelled activity.

Adapt - grants for individuals, groups and organisations to adapt their practice and explore new operating models.

Create - grants for individuals, groups and organisations to continue to create artistic work and develop creative responses in a time of disruption

Relief on grant conditions including removing requirements for meeting audience KPIs, bringing forward payments, delaying or simplifying reporting requirements, varying the purposes and outcomes of funding, extending timelines for projects, and allowing organisations to use project money to be repurposed to cover core costs

proceeding with Four Year Funding 2021-24, identifying how to keep as many organisations as possible funded through this critical period (details end of March)

Suspending investment programs currently or due to open, so as to concentrate on responding to the crisis. Programs which will be suspended include Career Development Grants, Arts Projects Grants, Fellowships, Touring and Travel Funds, Rights Fund for Literature, Translation Fund for Literature

Launching “Creative Connections,” an online webinar series offering practical, accessible and useful professional development including crisis management and communication, arts in the digital age, ongoing issues of climate change, intercultural working with First Nations artists and inclusive learning practices

Continuing the Arts and Disability Mentorship Initiative

Weekly First Nations roundtables

Weekly COVID-19 support workshop with peak bodies

New Facebook group “Arts and Creative Industries: Digital Support”, primarily a professional development and distribution resource

Click here for more info about the Federal government initiatives.

Click here for more info about the Australia Council for the Arts responses.

Click here for more info about the $27 million funding.

Click here for info about the public interest journalism funding advance.

Click here to find out what is happening at the State and local government-level in Australia.

Austria

Recovery Approaches

From 15 May, places of presentation such as museums, galleries and exhibitions, libraries, libraries and archives including reading areas have been allowed to reopen. Drive-in cinemas can also reopen. Stages will be as follows:

29 May: events with up to 100 visitors

1 July: events with up to 250 visitors

1 August: events with up to 500 visitors should be possible

Each event will need its own "corona manager". If a special security approach is available, events with up to 1,000 visitors can also be allowed. These openings only apply to events with seats, which must be at least one metre apart.

Emergency Support

Specific measures have been adopted by the Federal Ministry of Arts and Culture to cover the cultural sector:

Immediate aid may be granted to artists and cultural workers under the artists' social security fund. The COVID-19 fund has a maximum of 5 million euros and is intended to ensure rapid assistance. A total of up to 6,000 euros will be paid out - in the first phase up to 1,000 euros, in the second phase up to 2,000 euros per month for a maximum of three months;

The EUR 2 billion hardship fund (yes, 2 billion) has been set up as an emergency aid to all sole proprietorships, micro-enterprises (up to 9 employees), artists or newly self-employed people whose turnover has fallen as a result of the pandemic measures in the creative sector

Collecting societies have set up various programs for musicians, music labels, visual artists, filmmakers, audiovisual media, writers and translators, performers and producers of sound and video clips e.g. Collecting Societies of Music Austria has established EUR 2 million fund for creatives

In addition to state instruments to compensate artists for loss of income, there are private initiatives. To help artists in the current crisis, foundations have joined together to form the initiative "Foundations help artists."

The Ministry for Arts, Culture, the Civil Service and Sport has established a EUR 700 million fund for non-profit organisations.

The Ministry has also increased film subsidies by EUR 1.2 million, cinema subsidies by EUR 0.5 million, publishing industry subsidies by EUR 0.8 million, EUR 0.42 million to the Austrian Music Fund, EUR 0.25 million for art acquisitions

The City of Vienna now offers independent artists and independent scientists with their main place of residence in Vienna the opportunity to apply for one-off work grants up to a maximum of 3,000 euros. In this crisis situation, it should be possible to continue to pursue artistic and scientific activity (project development, reading, preparation of exhibitions and conferences, etc.);

Other indirect support measures exist for cultural institutions and artists: reduction and deferral of social security contributions, tax relief.

On 13 May, the government also announced a corona aid fund of EUR 700 million for NGOs, including from the sports, arts and culture sectors. The fund will cover fixed costs for two quarters (six months).

Click here for more info.

Belgium

Recovery Approaches

The Belgian government has announced a phased reopening:

11 May: Museums, libraries and bookstores re-opened; resumption of youth activities

8 June: Some cultural activities with audiences can resume

1 July: Performances with then public, including cinemas, can resume, always according to specific audience management rules – social distancing and max. 200 people, and avoid large gatherings

1 August: gatherings such as festivals can resume gradually, but major mass events will be banned until 31 August

Digital Actions

Culture at home is an online portal supported by the Federation Wallonie-Bruxelles Ministry of Culture. It provides links to offerings from cinemas, lectures, performing arts, museums and other initiatives.

Emergency Support

Belgium announced:

The Flemish government has announced:

a one-off premium of EUR 4,000 for entrepreneurs who have had to close their location

additional premium of EUR 160 per mandatory closing day beyond 5/4/20

compensation premium of EUR 3,000 (up to 5 premiums) for companies who are allowed to continue working but have experienced a 60% turnover decrease between 15/3 and 30/4

bridging loans and medium-term loans, postponement of loan payments

extension of grant deadlines

Click here for more info.

The Wallonia-Bruxelles Finance minister set up a EUR 50 million fund on 19 March to help culture, early childhood, sport, youth, education and university hospitals. Most of this first emergency fund will go to culture and early childhood. This fund will come to the rescue of cultural and associative activities that cannot take place because of the confinement, but for which the remuneration of artists and entertainment professionals must nevertheless be ensured. An online platform will be launched on 6 April in order to gather all the information and procedures to get some support.

On Tuesday 7 April, the Belgian government approved the proposition of the Ministry of Culture to dedicate over EUR 8.4 million for the support of cultural actors that have been impacted by the cancellation of activities and closure of venues. You can find the press release here on the website of Fédération Wallonie-Bruxelles.

Burkina Faso

Recovery Approaches

We are not aware of any announcements as at 11 June 2020.

Emergency Support

The Minister of Culture, Arts and Tourism announced the creation of a 1.25 billion CFA francs (US$ 2.1 million) fund, for the benefit of cultural actors, stressing that, in addition to this sectoral measure, cross-cutting economic measures relating to the economy as a whole have been taken by the President, providing for support for other sectors that have suffered harm as a result of COVID-19, including tourism.

Click here for more info.

Canada

Recovery Approaches

We are not aware of any announcements as at 11 June 2020.

Digital Actions

The Canada Council established the Digital Strategy Fund for grants of up to CA$50,000 for short-term activities. From April to 31 July, artists, groups and organisations can submit proposals that will:

· implement digital solutions as a strategic response to the COVID-19 crisis

· demonstrate concrete and immediate benefits to the arts community

· show elements of openness and potential for growth as a long-term strategy

On 21 April, CBC/Radio-Canada and the Canada Council for the Arts announced the creation of Digital Originals, a new time-limited funding initiative to help artists, groups and arts organizations pivot their work for online audiences during the COVID-19 pandemic. The fund offers CA $5,000 micro innovation grants.

The funding will directly benefit creators of original digital content. The Canada Council is providing CA $1 million in funding to successful applicants to develop, create and share original or adapted works with Canadian audiences online.

CBC/Radio-Canada will showcase and amplify the discoverability of select projects on one or more of its platforms. Selected projects for the curated CBC-Radio/Canada showcase will receive a supplemental amount of $1000. With the sponsorship of the RBC Foundation, as part of their ongoing activities to support youth in Canada, $150,000 in Digital Originals funding is available for new and early career artists.

Emergency Support

On 17 April, the Canadian government announced a further CA $1.7 billion in targeted measures for the economy, including CA $500 million to establish a COVID-19 Emergency Support Fund for Cultural, Heritage and Sport Organisations. In Phase 1, the Canada Council will distribute CA$55 million to eligible arts organisations experiencing a significant financial impact as a result of the pandemic.

On 30 March, the Canada Council for the Arts announced CA $60 million in advance funding, equivalent to 35% of annual grants held by over 1,100 core funded organisations.

By 4 May, the Council will issue advances enabling core funded organizations to: meet their immediate commitments, help ensure cash flow and address outstanding payments to the artists and cultural workers they employ.

The Canada Council is also:

Suspending funding for public events and travel-related activities

Allowing grantees to postpone events / travel or move events online

Apply grant funding to eligible expenses, including modifying, postponing or cancelling an activity

Core funded organisations will not be required too have replacement programming for events or activities

No penalties for not meeting current reporting deadlines

Extending some deadlines and continuing to run grant assessments

Relaxing repayment of grant rules:

For grants $5,000 and under

For grants between $5,000 and $30,000

For grants between $30,000 and $75,000

For grants above $75,000

The National Arts Centre with Facebook and Slaight Music has set up the Facebook-National Arts Centre Fund for Performing Artists, allocating $200,000 in artist fees to support live performances. The fund pays $1,000 to each act for their live-streams performances. #CanadaPerforms

Typically, self-employed people may not have access to employment insurance or sick leave. The Canada Revenue Agency will provide:

Emergency Care Benefit for workers and parents without paid sick leave. People who are not eligible for Employment Insurance and can’t access sick leave can also receive up to $900 every fortnight for 15 weeks if they are off work to take care of others.

$5 billion for an Emergency Support Benefit to workers who are not eligible for Employment Insurance and have lost their jobs or have reduced hours because of COVID-19. This includes artists and cultural workers. People can apply in April though the CRA website. It refers to a GST-credit payment of $400 to individuals and about $600 for couples; an increase in the Canada Child Benefit of $300 per child; and a 10% wage subsidy for small businesses for 3 months, up to $2,000 per employer.

Small businesses can receive a temporary wage subsidy for three months, equal to 10% of remuneration for that period, up to a cap of $1,375 per employee and $25,000 per employer. Businesses can access this immediately by reducing their income tax remittances.

Click here for more info about Canadian government initiatives.

Click here for more info about the Canada Council’s response.

Click here for more info about the National Arts Centre Facebook initiative.

Chile

Recovery Approaches

We are not aware of any announcements as at 11 June 2020.

Digital Actions

The Chilean government supports the online culture portal, Elige_Cultura. The website aggregates links to cultural offerings from across artforms, including museums, cinema, literature, visual arts, performing arts and music.

The Ministry of Culture is also offering a range of online capacity-building workshops for the cultural sector.The Ministry of Culture, Arts and Heritage has allocated CLP $15 billion to support copyright payments, promote artistic creation, and protect cultural spaces and organisations affected by the pandemic. The funds are from a repurposing of existing programs and instruments.

Emergency Support

The Ministry is also continuing to pay 2020 Culture Funds and is suspending Open Windows so artists do not incur expenses on activities that cannot be carried out. Once the pandemic crisis is over, these calls will be replaced. The Ministry is also working on specific measures for the regions and running a survey of the sector.

Click here for more info.

Colombia

Recovery Approaches

We are not aware of any announcements as at 11 June 2020.

Digital Actions

The Ministry of Culture has launched the #CulturaDigital strategy and allocated COP $24 million to the call for ‘share what we are’. The Ministry is also creating a national registry of artists.

The digital strategy includes access the free films, children’s content, museums online, theater, dance, arts, science and literature. #CulturaDigital and #QuédateEnCasa

Emergency Support

The Colombian Ministry of Culture has announced:

COP $80 billion for social security for older artists and cultural managers through the Periodic Economic Benefits Scheme

COP $40 billion for creation, virtual training, production and circulation of public performances of the performing arts, face-to-face or virtual, for the next 18 months

Extension of deadlines for taxes and fees and funded events

On 31 March the Minister of Culture also announced a new mechanism to assist artists and managers who are not eligible for other government social programs. They will receive a grant of COP $160,000.

The government has also implemented a fiscal incentive to leverage COP $30 billion in investments and donations for creative economy projects, including arts and heritage, and has established tax benefits and exemptions for artistic and cultural organisations.

Click here for more info.

Croatia

Recovery Approaches

The Second Package of measures announced in May aims to encourage and restart cultural life and promote the production and distribution of cultural and artistic content:

On 28 May, the Ministry launched Entrepreneurship in Cultural and Creative Industries which focuses on adapting business models and covers the fields of performing arts, literature, publishing and book activities, visual arts and audiovisual activities. The total amount of funds allocated for this program is 8 million Kuna

Additional funds will be provided for co-financing films

The Ministry of Culture is in the process of adopting a State Aid Program to support entrepreneurs in culture and creative industries and facilitate access to finance for small and medium enterprises

The Ministry of Culture will consult with the organisers of events and festivals, as well of other beneficiaries of support in order to approve new programs and budgets

Support to the performing arts and cinema industry who have been unable to launch activities due to restrictions is under discussion

Digital Actions

18 May, as part of the second package, the Ministry published the call Art and Culture Online, with a total grant of 25 million Kuna to finance the preparation and implementation of online artistic and cultural activities.

Please click here for more info (In Croatian)

Emergency Support

In March, the Ministry of Culture of the Republic of Croatia adopted measures to minimise the adverse effects of the COVID-19 pandemic and to protect cultural values. The Croatian Ministry of Culture has established a Crisis Fund (EUR 6.3 million) which will include funds for cultural workers whose projects have been delayed. Those who have lost their work due to the crisis will be given grants up HRK 1,625-3,250 for a period of three months from 1 April.

The First Package, adopted during the suspension of all cultural activities includes:

The postponement of contracted programs and conditions of payment for approved programs

Measures for job preservation

A public call to support professional artists who perform independent artistic activity and whose contributions are paid from the budget of the Republic of Croatia

A special fund for independent professionals who do not have a regulated status

The Croatian government is also supporting entrepreneurs in the cultural and creative industries, and self-employed artists, through the Croatian Employment Service. Small and micro loans for entrepreneurs and special support programs for sole traders are also being developed.

Please click here for more info. And if anyone can read this language, please correct me - I was using Google Translate!

Cuba

Recovery Approaches

We are not aware of any announcements as at 11 June 2020.

Digital Actions

The Cuban Institute of Music (Instituto Cubano de la Música), in collaboration with the Ministry of Culture and the Cuban Institute of Radio and Television, promoted online concerts via social networks as well as radio and television. The virtual concerts started on March 15 and continued throughout May. They included performances by a range of musicians in support of the national campaign #EstamosContigo#MusicosPorCuba to stop the spread of Covid-19.

Emergency Support

On 6 April the Ministry of Culture announced that artists who are part of the Cuban Institute of Music and the National Council of Performing Arts will receive salary support. The salary coverage begins in April, to be paid in May ,and will be effective through the usual payment mechanisms.

Click here for more info.

Cyprus

Recovery Approaches

As of 9 June, Cyprus entered phase three of the gradual easing of lockdown restrictions. Attendance at cinemas, theatres, indoor performances, mass and other events such as festivals, remain banned whereas the operations of services such as restaurants, cultural clubs and associations are permissible but subject to the guidelines offered by the Ministry of health. For specific details click here.

Emergency Support

On 7 April, the Minister of Education, Culture, Sports and Youth announced:

subsidies for salaries in cultural organisations whose work has reduced by at least 25%

suspension of loan payments

advance payments of cultural grants for activity to be undertaken in Q1 2021

expenses already incurred for cancelled events will be covered where appropriate

EUR 1.045 million allocated to the four Literary and Artistic Houses, the two Dance Houses and the Rialto Theatre

requests will be considered for damages incurred during filming/pre-production

increasing by 50% the amount provided for the Purchase of Art Works for the State Collection

Financially enhancing the cinematic projection of European producers

Encouraging and promoting online film and AV activity in short films, documentary and animation

Looking at how to support theatre professionals

For more info click here.

Czech Republic

Recovery Approaches

We are not aware of any announcements as at 11 June 2020.

Emergency Support

The Ministry of Culture has established:

a EUR 16.1 million support fund for those in the all-year subsidy groups of dance, theatre, music, visual arts and small publishers.

EUR 1.1 million call for multimedia platform projects in experimental forms

EUR 10.1 million for arts organisations, museums and galleries

The City of Prague has also announced:

Click here for more info.

Denmark

Recovery Approaches

Denmark’s cultural life will reopen in stages (Phase 1 related to schools reopening).

Phase 2

11 May Resumptions include lending at libraries, artistic programs such as music exams that require a physical presence, professional sports, outdoor sports and associations, visits to zoos by car, art centres, museums, theatres and cinema’s

May 27 Openings include music and cultural schools, colleges and evening schools, summer activities for children and young people

Phase 3

Phase 4 , beginning of August

Resumptions include those parts of the artistic education that were not opened in phase two, venues, additional indoor sports and leisure activities

Bans on events and activities of more than 500 people will continue until at least 31 August

For further details click here (In Danish)

New Laws and Regulations

For information on new laws and regulations that have resulted from COVID 19 click here (In Danish)

Cultural assistance for Senior Citizens

10 Million DKK has been made available to provide cultural assistance to the elderly affected by COVID 19. Initiatives such as collaborations between cultural and social actors with nursing homes and municipalities will be considered. Further details are available from the Danish Ministry of Culture (in Danish).

Emergency Support

On 18 April the Danish government announced an emergency pool of DKK 200 million for distressed public-oriented cultural institutions and seasonal performing arts companies which fall through other relief packages. The fund is for institutions with operating grants from the Ministry of Culture and can cover:

up to 80% of production costs for performances and exhibitions etc

these institutions can be further compensated if they are particularly distressed, to prevent otherwise well-run institutions to go bankrupt. The compensation may not exceed 80% of lost revenue

municipal cultural institutions with Ministry of Culture operating grants and six larger municipal venues can receive salary compensation and compensation for fixed expenses

distressed performance events etc which are not covered by the general event pool can be compensated for up to 80% of expenses from 9 March to 31 August.

The Danish government has previously announced:

Compensation for companies’ fixed costs

Compensation for self-employed persons who experience more than 30% decrease in revenue as a result of COVID-19. The government will provide 75% of the loss of revenue, up to a maximum of DKK 23,000 per month, for three months. The compensation may amount to DKK 34,500 per person per month if the self-employed person employs their spouse. This is targeted at sole traders and companies employing fewer than 10 employees.

Support for private companies to keep workers on furlough

Compensation if you had to cancel an event from 6-30 March for more than 1,000 people (or 500 people if the event was targeting COVID-19 high risk groups)

Temporary deferral of tax payments

On 6 April the Danish government also announced a temporary art support scheme for artists with ‘A and B income’ and taxable profits from self-employment of at least DKK 8,333 monthly on average. The scheme is estimated to cost DKK 100 million kr. Artists can apply who:

have a total A and B income and taxable profits from independent artistic activities of between DKK100,000-800,000 annually, corresponding to DKK 8,333-66,667 monthly on average in one out of the past three years, based on annual reports from 2017 ,2018 and 2019.

expect a loss in A and B income and taxable profits from self-employment from the artistic activity of at least 30%. 75% can be covered of the expected loss to a maximum of DKK 23,000 per month

In a press release 15 May, ( in Danish) it was announced that the government would extend aid packages to the temporary art support scheme for artists for an extra month until July 8, 2020.

For more information click here. And correct me if you know Danish - this is courtesy of Google Translate.

Click here for info about the art support scheme and click here for information about the 200 million kroner emergency pool.

England

Recovery Approaches

The Covid-19 recovery strategy is as follows:

Step one, 11 May: Those who cannot work from home will be encouraged back to their workplaces, exercise will be unlimited, sports may be played with household members, able to drive to other destinations.

Step 2, 1 June: People may leave their house for any reason, up to six people may meet outside, some schools will resume, shops subject to closure will reopen on 15 June.

Step 3, at the earliest from 4 July: The government hopes that some parts of the hospitality industry and other ‘public places’ will be able to reopen ‘provided they are safe and enforce social distancing’.

Digital Actions

BBC Arts with Arts Council England has launched a new commissioning strand “Culture in Quarantine Fund,” which will support England-based artists of any discipline to produce new works in creative media – video, audio and interactive – in spring 2020. Grants will be in the range of £3,000-8,000 (ex VAT).

The Arts Council already has a program called the “Digital Culture Network,” which employs “Tech Champions,” who can help artists and organisations to develop their digital skills.

Emergency Support

The UK government is offering:

Cash grants up to 25,000 pounds for retail, hospitality and leisure businesses through the Retail and Hospitality Grant Scheme

Taxable grants of 80% of profits for a self-employed person or member of a partnership who has suffered a loss of income from COVID-19, up to a cap of 2,500 pounds per month. The Coronavirus Self-Employment Income Support Scheme is open to those with a trading profit of less than 50,000 pounds and with a full year of accounts.

‘Business rates holiday’ for retail, hospitality and leisure businesses in 2020-21.

For businesses that are too small to pay much in the way of business rates anyway, the government will provide Small Business Grant Scheme funding for local authorities, which will provide one-off grants of 10,000 pounds to eligible businesses to meet ongoing costs.

Temporary tax relief for self-employed people and businesses, including deferral of VAT and income tax payments for the self-employed until January 2021.

Coronavirus Business Interruption Loan Scheme, to support small and medium-sized businesses to access loans and overdrafts. Government will provide an 80% guarantee on each loan and the Scheme will support loans of up to 5 million pounds first 12 months interest free.

Coronavirus Job Retention Scheme to provide up to 80% of furloughed workers wage costs, up to a cap of 2,500 pounds per month.

Statutory Sick Pay refund for up to two-weeks of employees’ sick pay for businesses with fewer than 250 employees.

Access to Universal Credit (income support), suspending the minimum income floor restriction and removing requirement to go to a job centre

Access to Employment and Support Allowance (if you have a health condition which prevents you from working), if you have paid National Insurance contributions over last 2-3 years

In the next wave of emergency funding, Arts Council England announced 160 million pounds in an emergency funding package which includes:

90 million pounds available to national portfolio organisations and creative people and places consortia

50 million pounds for organisations which are not regularly funded but have a track record in receiving public funding, with the aim of addressing cashflow challenges and commissioning work now, to be available to people during the crisis, thus supporting artists as well. Disabled-led organisations will be prioritised, as will organisations’ capacity to deliver “Let’s Create” after the crisis, which includes consideration of whether the organisation is diverse-led.

20 million pounds for individuals who are creative practitioners in music, theatre, dance, visual arts, literature, combined arts and museums practice fields (magicians and comedians can apply if they have a track record of receiving public funding); 4 million pounds of this will be grants for benevolent funds targeted at other cultural workers. This is based on the calculation that in place of a single 10,000 pound grant from the “Developing Your Creative Practice” fund, ACE could invest 2,500 pounds in four different artists, helping them through the crisis. There is a higher application ceiling (3,000 pounds) for disabled and D/deaf applicants to factor in additional support needs

The Arts Council is also:

Relaxing grant funding conditions.

Offering to advance six months of grant payments to national portfolio organisations and postpone the next national portfolio investment process, so that the current suite of organisations will roll over to 31 March 2023

Producing guidance in BSL, Large Print and Easyread, and running two rounds so anyone who needs more time can have it

Click here for more info about Arts Council England’s emergency package.

Click here for more info about the UK government economic response.

Click here for more info about the BBC Arts Culture in Quarantine program.

Estonia

Recovery Approaches

Conditions for organising events eased as early as June (in Estonian, 29 May)

1 June, the number of people allowed to attend public indoor events will increase from 50 to 100. The 2+2 and other requirements remain the same.

1 June to 30 June, Outdoor sports competitions may resume with a total of 100 participants. The organiser must ensure that disinfectants are available.

Emergency Support

The Estonian Ministry of Culture has announced an initial EUR 3 million to partially compensate for the direct costs and income lost due to the cancellation of cultural and sporting events and activities, which it increased to EUR 10.1 million. The Ministry of Culture is working with the Cultural Endowment and will launch this measure as soon as possible.

On 22 April, a temporary amendment to the Creative Persons and Creative Societies Act was passed, which aims to support creative practitioners who have lost their income. A minimum wage is guaranteed for six months and is available to freelance creative practitioners who are creators as defined in the Creative Industries Act and whose main source of income is professional creative activity in the fields of architecture, audiovisual, design, performing arts, sound, literature, visual arts. The Ministry of Culture applied for an additional EUR 4.2 million to cover this expansion of the Act to a total of approx. 1,200 people who work in creative fields and have been disrupted by the pandemic.

Easing of restrictions include:

allowing someone who has already accessed support in the last two years to receive benefits

the requirements for income earned in the previous month has been amended

creative practitioners who do not belong to a recognised creative union, but who met the requirements of the Act, can apply for a creative grant from the Ministry of Culture

creative practitioners can continue to earn additional income while receiving the grant

These measures are part of a larger government package of EUR 2 billion in stimulus measures. For more information, visit the Estonian Ministry of Culture (in Estonian, dated 25 March).

Finland

Recovery Approaches

On 11 June, the Government announced that partial border control will continue at internal borders while external border traffic will continue to be restricted until 14 July 2020.

15 June, 14 day self-isolation is recommended for all those arriving in Finland from countries that are still subject to internal or external border control.

For further information click here (in Finnish)

The Finish government website lists the following information in regard to re-opening of cultural facilities;

Museums, theaters, the National Opera, houses of culture, libraries, hobby facilities and venues, as well as youth and club facilities can be opened from the beginning of June.

Concerts, theater performances, festivals and other cultural events are public events. They must take into account the current maximum number of participants of 50 or, by special arrangements, 500.

Public events of more than 500 people are prohibited until 31 July. For outdoor events with several auditoriums or demarcated areas for the public, it is possible to hold events for more than 500 people

Emergency Support

The government has established a fund for professionals in arts and culture of EUR 19 million., EUR 3.2 million for institutions, EUR 18 million for theatres, orchestras and museums, and EUR 1.3 million for the Governing Body of the Suomenlinna and the Finnish Heritage Agency.

The Ministry of Culture, the Ministry of Education and Culture, and the Finnish Centre for Art Promotion will jointly provide rapid support to arts and cultural professionals in distress due to COVID-19.

The Kone Foundation is offering a three-month work grant for artists residencies which take place in the artist’s home. It includes a monthly grant and an online work platform to share ideas. The size of the monthly grant varies according to the applicant’s experience: €2,400 (early career), €2,800 (mid-career), €3,500 (experienced artist).

Click here for more info.

The Finnish Cultural and Academic Institutes network has announced a new grant program “Together Alone - Open Call”. The Institutes are seeking artistic proposals related to the following themes: state of emergency, radical change, resilience, artistic practice in the future, alone together. At the same time the project will act as a documentation of the crisis, and one of the major social upheavals of our time and give the artists an opportunity to reflect it through the arts. The application is open to all Finnish and Finland-based professional artists who have lost work opportunities due to the corona epidemic.

The Institutes are commissioning projects from selected artists or artistic groups to be completed by June 30, 2020. The total grant of an individual project is between EUR 1500–5000.

The aim of the open call is to ensure the livelihoods of artists, and the continuity of international collaboration. Although mobility and physical encounters must now be restricted, we want to support the international networks and cooperation.

Click here for more info.

France

Recovery Approaches

On 6 May the French Minister for Culture detailed measures to support the resumption of cultural life (in French)

11 May, bookshops, record stores, libraries, media libraries and art galleries may reopen, along with certain museums and historic monuments

The rights of artists and intermittent performing technicians, who have been sanctuarized for three months, will be extended by one year until the end of August 2021

A guarantee fund of EUR 50 million will be allocated for the filming of cinematographic and audio-visual productions, to compensate producers for “Covid-19 risks”

An endowment of EUR 50 million has been allocated to the National Music Centre to support the entire music industry.

AVMS (audio-visual media services) and copyright directives will be transposed into French law before the end of the year to better protect, from January 1, 2021, audio-visual companies within the cultural sovereignty framework

A global public order plan will be launched in each cultural area

The artistic presence will be reinforced via cultural education and there will be a launch of a new initiative, "A learning summer", in July and August 2020.

Resumption of Activity in the Cultural sector

14 May, Ministry of Culture ( in French) announced that, while guides for the cinema and artistic creation sectors are being finalised:

Museums and monuments may reopen as they are not likely to encourage significant displacement of the population

Theatres and cinemas will remain closed. Likewise, festivals and cultural events bringing together more than 5,000 people cannot be held until August 31.

Specific details in regard to health and safety details will be posted here (in French) as they become available.

Emergency Support

France has announced 45 billion euros in overall action, which includes:

unemployment benefits for people forced to work part-time

a ‘solidarity fund’ of 2 billion euros to help shopkeepers and the self-employed

Paying small and medium businesses to keep workers on furlough

Bank loan guarantees for businesses and tax deferrals

For the cultural sector, on 18 March the Ministry of Culture announced an emergency fund which will include in its first phase EUR 22 million, which includes EUR 10 million for music, EUR 5 million for entertainment, EUR 5 million for literature and EUR 2 million for visual arts.

The Ministry will:

count the period that contract-based cultural workers are unable to work as part of the reference period which gives entitlement to unemployment insurance

pay unemployment insurance benefits for contract-based cultural workers even if their entitlement was set to end during the current period

On 27 March the Ministry also announced additional measures for artists to receive an individual support grant of up to EUR 1,500.

Click here for more info.

In France there are a number of agencies which oversee specific sectors, including specific sector taxes.

The National Music Centre has:

established an 11.5 million euro emergency fund for the entertainment industry, particularly small and medium enterprises. Each grant, capped at € 11,500, includes an incentive to pay artists compensation for canceled shows.

suspended the payment of ‘show tax’

The National Centre for Cinema and Animated Image:

suspended the entry tax in cinemas for March 2020

is providing financial aid to art house infrastructure and softening criteria for accessing aid

Grants already awarded for cancelled events will be paid and not required to be paid back

The performing arts sector outside music has had up to 5 million euros allocated for emergency aid.

The National Book Centre is implementing:

an emergency plan with a first envelope of 5 million euros to respond to the immediate challenges of publishers, authors and booksellers: 1 million euros for direct social aid to book authors, 0.5 million euros to French-language bookshops abroad; 0.5 million euros for the most fragile independent publishing houses; and intervention fund to compensate for operating losses of bookshops.

subsidies already paid to book events cancelled because of the pandemic will not be required to be repaid, with particular attention to payment of authors who would have appeared at the events.

the Centre is also postponing the maturities of loans granted to booksellers and publishers.

The National Centre for Plastic Arts has:

an initial 2 million euro fund for art galleries

expanded eligibility for gallery grants

support allocated to galleries to attend postponed fairs will not have to be repaid

The Minister of Culture and the Minister of Labour are working on specific measures for freelance performers and technicians and creators.

At the regions level, governments are planning to support canceled events up to the amount of costs incurred. For example:

the Ile-de France region has announced an emergency aid fund of 10 million euros for the performing arts

The New Aquitaine region has committed to the national fund and also reserved 5 million euros for associations in the form of direct grants in culture, sport and the social sector

The Pays de la Loire region has announced an emergency plan of 50 million euros for businesses in the cultural, sports and community sectors (25 million euros of immediately available loans through existing mechanisms, and 25 million euros of new measures and loans, including 2 million in support of cultural and sports associations, which can be leveraged to grant 325 million euros in loans in the Loire region).

This also includes a 6 million euros in cash subsidy for artisans, traders, restaurateurs, very small businesses and social enterprises

Rebond loan for SMEs of zero-interest of 10,000-300,000 euros

Postponement of repayable advances granted by the regional government due for the next 6 months

loan guarantee scheme increased to 80% (from 70%) aimed at very small businesses and SMEs

unsecured cash loans of 50,000-500,000 euros at a TEG rate of 2.03%

Emergency Events Fund aimed at all associations organising cultural and sport events hard hit by cancellations / drop in attendances due to the pandemic, with a grant ceiling of 30,000 euros.

For more info click here about the general economic package.

Click here for more info about the French Ministry of Culture announcements and feel free to correct me as I used Google Translate on this.

Click here for info about the National Music Centre fund.

Germany

Recovery Approaches

The reopening pf public life and social distancing

6 May, specific details on the federal and state governments restrictions on public life and social distancing can be found here. In general, social distancing and hygiene rules still apply and certain institutions such as schools will gradually open. The federal states will need to determine schedules for the reopening of theaters, operas, concert halls and cinemas.

To watch a video of Chancellor Angela Merkel discussing steps to ease the coronavirus lockdown click here.

NEU START

In a press release (in German) on 4 June, the German government announced that around one billion euros would be made available to the cultural sector via the Neu Start initiative. This funding will cover 2020 and 2021. The Neu Start program is divided into four parts:

Pandemic-related investments in cultural institutions of up to 250 million euros, to make cultural institutions such as cultural centers, music clubs, theaters, cinemas, trade fairs, literary houses fit for the reopening. This includes measures such as the implementation of hygiene concepts and distance rules, online ticketing systems, the modernization of ventilation systems, different visitor guidance and seating, installation of protective devices, optimization of visitor control, public safety instructions,procurement of cleaning and infection protection equipment, measures to expand IT infrastructure, technical and other equipment

Maintenance and strengthening of the cultural infrastructure and emergency aid. This is the largest component of the program with a total of up to 450 million euros. Its purpose is to aid small and medium sized cultural sites and projects who have lost revenue but still have to pay staff. This part of the project also focuses on placing new orders with freelancers and solo professionals.

Promotion of alternative, also digital, offers. See Digital Actions below.

Pandemic-related additional needs of up to to 100 million to compensate for corona-related loss of income and additional expenditure that cannot be covered in any other way. The package also provides for federal aid of 20 million euros for private radio broadcasters.

For a direct link to the Neu Start website click here.

Digital Actions

EUR 150 million in ‘New Start Culture’ funding (see above) will be made available to alternative and digital projects that serve to convey, network and communicate in the cultural field.

For further info click here.

Emergency Support

Germany has announced a huge 750 billion euros in stimulus, which includes EUR 50 billion euros for the cultural, creative and media sector, including freelancers and small businesses, including artists and caregivers. They are eligible for up to 15,000 euros in direct subsidies over a period of three months. They should be able to apply quickly and with little bureaucratic effort for subsidies to secure their professional or business existence.

At the State level:

The State of Berlin is providing short-term budget funds to mitigate the worst hardships for self-employed persons and small businesses in the private cultural sector, freelance and solo artists and cultural workers, honorary staff, small art associations and self-employed event organizers.

The State of north Rhine-Westphalia is offering EUR 5 million in emergency aid for artists.

The State of Hamburg: EUR 25 million for cultural institutions and EUR 50 million stimulation package by the Hamburg bank for cultural businesses

Municipality of Cologne: EUR 3 million emergency fund for ‘free culture’

Click here for more info.

Hong Kong

Recovery Approaches

We are not aware of any announcements as at 11 June 2020.

Emergency Support

Hong Kong has announced:

$1,200 cash subsidy to all adult permanent residents

cutting payroll, income, property and business taxes

low-interest, government-guaranteed loans for businesses

The Hong Kong Arts Development Council has also launched the HKD $55 million “Support Scheme for Arts & Cultural Sector” to support small and medium organisations and arts practitioners whose activities and work were cancelled or impacted in 2019-20. Under the Scheme:

Grant recipients of HKADC’s 2019-20 Year Grant, Literary Arts Platform Project and Eminent Arts Group Scheme can each apply for up to $130,000

Projects funded by HKADC through the Project Grant (non-publication) and Matching Fund Schemes will receive a direct subsidy of $15,000 and can apply for up to $15,000 further

Projects funded under the Project Grant (publication) stream will receive a direct subsidy of $3,000 and can apply for up to $3,000 further

Projects funded by HKADC under the Cultural Exchange Scheme, and commissioned projects will receive a direct subsidy of $15,000

Arts projects not funded by HKADC may receive a subsidy of $15,000 by application

Individual art practitioners may receive a maximum of $7,500 by application

HKADC extended the scheme for two more months, originally from 29 January to 30 April now extended to 30 June.

Click here for more info.

Indonesia

Recovery Approaches

We are not aware of any announcements as at 11 June 2020.

Emergency Support

On 11 May, the Yogyakarta regional government received permission from the central government to use the ‘Privileged Fund’ (Danais) to deal with COVID-19, including a fund of RP 600,000 per month to artists and cultural workers affected by the pandemic.

Click here for more info.

Ireland

Recovery Approaches

16 June, the government announced EUR 25 million recovery package to support the arts and culture sector recover from the COVID-19 emergency. The funding will include bursaries and commissions to artists and arts organisations, and resources for museums and culture workers as they prepare for the reopening of society.

A total of EUR 20 million will be allocated to the Arts Council bringing its allocation this year to EUR 100 million.

Priority areas for the extra funding include averting the closure of key organisations, expanded commissioning schemes for individual artists and arts organisations across all art forms, and expanded bursary schemes, open to artists and groups of artists to develop their professional practice.

Separately, EUR 5 million has been set aside for measures including securing the future of key cultural and museum spaces and the production of high-quality digital art and online performances.

18 May, The Arts Council of Ireland announced the publication of guidelines for reopening of arts centres:

Phase 2: 8 June Phased return of workers

Phase 3: 29 June Return to organisations of employees who have low levels of daily interaction and where social - distancing can be maintained.

Phase 4: 20 July Return to organisations of employees who cannot work remotely. The re-opening of museums, galleries, and other cultural outlets - where people are non-stationary and social distancing can be maintained.

Phase 5: 10 August Resumption of 'Higher risk' organisations which by their nature cannot easily maintain social distancing. Plans are to be implemented on how they may progress towards onsite return of full staff . This will include the re-opening of theatres and cinemas where social distancing can be maintained.

The Irish government have a dedicated COVID-19 information page for further information, advice and guidelines which isupdated daily.

Digital Actions

3 April, Ireland and Culture Ireland will match funding of €100k support with Facebook Ireland for the online showcasing of artists’ work.

The Department of Culture, Heritage and the Gaeltach is partnering with RTÉ, TG4 and others to bring a broad range of cultural, heritage and language content to the public from archive as well as new sources in partnership with organisations such as Druid and Other Voices.

Emergency Support

The Department of Employment Affairs and Social Protection is offering a COVID-19 Pandemic Unemployment Payment for people who have lost work due to a downturn in economic activity caused by the crisis. This delivers income support to the unemployed, including self-employed people, for six-weeks. During this period, you can apply for a full Jobseekers payment and receive any additional entitlements backdated.

Those diagnosed with COVID-19 or who have to self-isolate can apply for the Illness Benefit for COVID-19 absences paid at 305 euros per week. This is available to employees and the self-employed.

On 3 April the Arts Council Ireland launched a EUR 1 million fund ‘Arts Council COVID-19 Crisis Response Award,’ to support the creation of new artistic work and its dissemination online for the public benefit.

The Arts Council is also creating a new digital platform so people can experience artworks in their own homes

The fund will be made up of 50% from the Arts Council’s existing budgets, and 50% from the Department of Culture, Heritage and the Gaeltacht

Successful applicants will be awarded EUR 3,000.

Other initiatives include:

Department through Culture Ireland match funding EUR 100,000 support with Facebook Ireland for the online showcasing of artists’ work

Partnering with RTE, TG4 and others to bring cultural content to the public from the archive and new sources in partnership with organisations such as Druid and Other Voices

Abbey Theatre commissioning writing and performance of 50 new monologues during April

a new Creative Ireland partnership with Healthy Ireland to promote wellbeing and creativity, including sharing of new Design & Crafts Council Ireland online resources to engage young people and adults in home-based making activities

TG4 to partner with Comhaltas Ceoltóirí Éireann for a reimagined Fleadh Ceoil and TG4 Molscéal to showcase language-based Arts and stories from Gaeltacht communities in collaboration with Ealaín na Gaeltachta, TechSpace and others

The Arts Council has also previously said that:

It will honour all funding commitments and allow grantees to draw down 90% of their funding to allow them to fulfil their commitments, especially contracts with artists.

There will be no penalties for grantees who cannot deliver key activities because of COVID-19.

Click here for more info about the COVID-19 unemployment benefits.

Click here for info on the new Crisis Response Award.

Click here for more info about Arts Council of Ireland’s response.

Italy

Recovery Approaches

Phase 2

As at 1 June, the Italian government website lists the following guidelines in regard to the resumption of cultural activities:

Shows at theatres, concert halls, cinemas and other open spaces will remain suspended until 14 June 2020. From 15 June 2020, these shows will be held with pre-assigned and spaced seats and compliance with the interpersonal distance of at least one meter with a maximum number of 1000 of spectators for outdoor performances and 200 people for shows indoors.

Activities that take place in dance halls and discos and similar establishments, outdoors or indoors, fairs and conferences remain suspended.

Click here for further information (in Italian)

Emergency Support

Italy has announced EUR 25 billion in stimulus including:

For the cultural sector:

EUR 130 million in 2020 in the Live Show, Cinema and AV Emergency Fund for the support of cultural workers. The Minister for Culture and Tourism will determine how to allocate the fund

Refunds with vouchers for tickets to shows, cinemas, theatres and other cultural venues and hotels

Workers in tourism, culture, entertainment, film and AV sectors can access extraordinary allowances

Social safety nets are extended to seasonal workers in tourism and entertainment and interventions in favour of authors, artists, performers and agents

Suspension of withholding tax payments, social security and welfare contributions and compulsory insurance premiums for those who manage or organise venues, cinemas, museums, arts events, libraries, archives, historical monuments, bars, restaurants, spas, amusement or theme parks, transport services, rental of sports and recreational equipment or structures and equipment for events and shows, guides and tourist assistants

A campaign to relaunch ‘the image of Italy in the world’ for cultural and tourism purposes

Click here for more info about general actions.

Click here for info about cultural sector actions.

Ivory Coast

Recovery Approaches

We are not aware of any announcements as at 11 June 2020.

Emergency Support

The government has granted aid of CFAF 500 million to artists who are members of the Ivorian copyright bureau (BURIDA). As this is a distribution of rights, not all artists will benefit from it. CFAF 70 million has also been granted in food and non-food items to artists in Côte d'Ivoire in the form of withdrawal vouchers.

Click here for more info.

Japan

Recovery Approaches

Japan’s Ministry for Education, Culture, Sports, Science and Technology (MEXT) website states that as of 25 May the national emergency in Japan was lifted.

Japan’s Ministry of Health Labour and Welfare outlines in its Basic Policies for Novel Coronavirus Disease Control (Revised on May 25, 2020) their measures in combating COVID-19 including some general information in regard to holding events such as concerts, exhibitions, sports games, championships, festivals, etc.

Digital Responses

The Japanese Cabinet’s emergency measures include 1.4 billion JPY for digital content infrastructure.

Emergency Support

The Japanese government has announced:

The Cabinet also announced a supplementary budget on 7 April of 6.1 billion JPY (EUR 52 million ) to be allocated to the Agency for Cultural Affairs:

2.1 billion JPY (EUR 18 million) for measures against covid-19 aimed at reopening cultural institutions (support up to 4 million JPY (about 34,000 EURO)/case for expense such as installation of infrared camera device, disinfectant, etc. preparing for reopening)

1.4 billion JPY (EUR 12 million) for digital content infrastructure (see above)

1.3 billion JPY (EUR 11 million) for two projects called “Art Caravan” and “creating opportunity for children’s arts and culture experience” respectively.

The supplementary budget also includes an allocation of 87.8 billion JPY (EUR 750 million ) for “Global demand creation and promotion of content business”, a new joint project of the Agency for Cultural Affairs and Ministry of Economy, Trade and Industry.

Small and medium sized enterprises whose turnover has decreased by 50% compared to the previous year can apply to “Sustainable Benefits”: 2 million JPY (EUR 17,000) for corporate, 1 million JPY (EUR 8,500) for individual enterprise.

In the meantime, more specific measures to support freelancers in the arts and cultural sector are announced by municipal governments, such as Fukuoka City, which is supporting up to 500,000 JPY (EUR 4,300) per facility for live houses, halls, theatres etc attempting to distribute online contents and taking safety measures.

Click here for more info about loans and here for more info about culture measures.

Lithuania

Recovery Approaches

We are not aware of any announcements as at 11 June 2020.

Emergency Support

The Lithuanian Culture Council has created new funding measures as follows:

Individual scholarships for cultural or artistic creators: individual developers will be able to receive a 3 months scholarship for the development of individual creative activities. (>300 artists should receive this). This means that the second and third educational scholarship grant rounds are cancelled. Developers with relevant activities will be invited to submit for the new grant round.

Funding for cultural NGOs: EUR 1.2 million program for cultural organisations has been created (I think - this is via Google translate…)

Other grant programs are suspended until the end of the quarantine, and applicants will be invited to apply for the new funding measures

EUR 700,000 will be allocated from the Copyright and Related Rights Protection Program to compensate for losses incurred by cultural workers.

The Culture Council has also started talking to funded organisations about adjusting projects, reallocating funding and postponing some activities or reorienting others. These organisations will receive 100% of the 2020 funds rather than 90% this year.

Please see the Lithuanian Culture Council for more details.

Luxembourg

Recovery Approaches

We are not aware of any announcements as at 11 June 2020.

Emergency Support

The government of Luxembourg has amended its social assistance laws so that in the event of pandemics and terrorist attacks, the government has:

extending social assistance scheme to independent and freelance professional performing artists with the possibility of a monthly social assistance benefit up to the minimum social wage for qualified persons, and additional daily allowances (up to 20 per month)

reducing the income conditions normally required to be able to access aid schemes in proportion to the duration of the exceptional event (7 days per month during which the situation occurs)

grants for cancelled projects will not have to be repaid as long as the commitments to artists are still met for the most part

the Ministry of Culture will continue to fund new projects, with a focus on projects that can occur despite the pandemic, or requests from entities or artists in difficulty following the cancellation of a project

Cultural companies can also access partial unemployment benefits via the Employment Fund, which can cover 80% of normal salary (capped at 250% the minimum wage) for a most 1,022 hours per employee

Recoverable advances are also available to cover the loss of income of small and medium-sized enterprises and the self-employed

12 June, The Luxembourg Ministry of Culture announced an extension of its aid via the independent and intermittent professional performing artists scheme until August 31, 2020.

Click here for more info.

Malaysia

Recovery Approaches

We are not aware of any announcements as at 11 June 2020.

Digital Actions

Music from Home, an initiative of the Ministry of Communications and Multimedia Malaysia in collaboration with the Malaysian Music Committee, saw 300 artistes and musicians perform a series of virtual concerts on 8 April. The project provided a platform for artists to continue working and producing digital content to entertain their fans at home. Click here to read about this project (In Malay)

Emergency Support

The Communications and Multimedia Ministry (KKMM) has allocated RM1.32 million (US$302,884) as an Incentive Feature Film initiative (ITFC) in response to a proposal from the National Film Development Corporation Malaysia (Finas) to help film producers and encourage them to continue producing local films.

16 April A recovery programme introduced to support Malaysian artists, collectives and arts organisations

A new programme, called Create Now Funding, operating under the auspices of CENDANA (Cultural Economy Development Agency) will provide immediate response grants of up to RM 1,500 per individual artist/cultural worker and, RM 3,500 per collective/arts organisation.

Additional new grant programmes introduced by CENDANA include;

Visual Arts INSPIRE, to support exploration process and research excursion

Visual Arts SHOWCASE, to support the contemporary expression of visual art through independent, alternative and experimental art venues

Independent Music Funding Programme, which supports development and creation of new original or adapted works, live showcases and creation of digital content.

These programmes will be rolled out on April 14. For further information click here

Mali

Recovery Approaches

We are not aware of any announcements as at 11 June 2020.

Emergency Support

Fonds Maaya has established a Support Fund for Cultural Organisations to maintain organisations during the pandemic, with a maximum of FCFA 5 million per cultural organisation.

Malta

Recovery Approaches

We are not aware of any announcements as at 11 June 2020.

Digital Actions

17 May The Times Malta discusses the increase in online alternative used by artists, designers, curators and other visual arts practitioners including a proliferation of virtual exhibitions and projects launched on social media although they note that not all experiences translate to the screen and for some projects there have been some expensive delays

Emergency Support

The Arts Council Malta has announced that the government has supported a Self-Employed In Creative Arts COVID-19 Wage Supplement.

People working in the creative arts –whether full-time employees or self-employed/freelance – are entitled to a monthly supplement of EUR 800. Part-time employees within the creative artssector are entitled to a monthly supplement of EUR 500. An updated Wage Supplement scheme will remain in place until September 2020. The benefit rate from July 2020 will be EUR 800 for full-timers and EUR 500 for part-timers to support areas involved with tourist accommodation, travel agencies, language schools, event organisation and air transport. For more info click here

Creative practitioners working in the sectors which are originally considered to have been adversely, but not drastically, affected were to beentitled to a monthly supplement of EUR 160 in the case of full-time employees, EUR 100 in the case of part-time employees, and EUR 320 in the case of self-employed/freelancers. These sectors include publishing; motion picture, video and television programming; cultural education; photography and radiobroadcasting.

Furthermore, Arts Council Malta issued a special call for the Malta Arts Fund, the most established funding programme for the arts in Malta. This call provides a fund of EUR 75,000 for artists and practitioners to develop projects which address the cultural and creative sector as impacted by the situation. This call encourages artists to consider various pertinent themes – including borders, confinement and isolation – within their projects.

7 May, Arts funding scheme

EUR 75,000 has been awarded to 11 applicants as part of a special COVID-19 Arts Council Malta funding scheme, launched to address the financial impact of the pandemic on creative and cultural practitioners, groups and organisations.

Visit Arts Council Malta for updates (25 March).

Mexico

Recovery Approaches

We are not aware of any announcements as at 11 June 2020.

Emergency Support

The Ministry of Culture has:

instructed its cultural entities to allocate up to MXN $1 million for artists and local creators, totalling to up to MXN $32 million nationwide

announced a ‘function bank’ so that artists etc who were hired from March 20 to April 20 can receive payments on time and replace their presentations with remote presentations or postponements

offered up to MXN $200,000 for cultural programming and $1 million for cultural infrastructure renovations or equipment of buildings

offered up to MXN $5 million for financing cultural construction projects and equipping buildings

The Ministry has also opened a call entitled “With you in the distance: Art movement at home.”

Creators over 22 years of age, with a three year or more track record, can participate

Selected creators will receive MXN $20,000 in exchange for the dissemination of their work

Click here for more info.

Netherlands

Recovery Approaches

15 June. The Netherlands is taking a step by step approach to easing restrictions. The following outline measures relevant to the cultural sector:

Libraries are open, observing 1.5 metres social distancing measures.

Cinemas, theatres and concert halls can admit up to 30 people per auditorium (not counting staff) and must observe social distancing.

Museums and heritage sites may reopen with restrictions as to the numbers of visitors. Visitors must make reservations.

Music schools and arts centres can admit up to 30 people to their buildings incorporating social distancing measures.